7 Mistakes You're Making with Your Jewelry Insurance Valuation (and How to Fix Them)

As a jewelry appraiser and owner of Gemology Resources, I've been in the business since 1998 — working as a seller, buyer, appraiser, and repair manager. One thing I've learned is that most people believe their jewelry is "covered," but in reality they could end up with a much smaller payout than they expected.

An insurance policy is only as good as the document it's based on. If your valuation is flawed, your insurance company may not pay out what you expect, or worse, they may replace your heirloom with a vastly inferior stone. You must understand that a valuation is not just a price tag; it is a legal and technical document of your property.

Here are the seven most common mistakes I see in my Houston office and, more importantly, how you can fix them before it's too late.

1. Relying on a Sales Receipt as an Appraisal

The mistake? They submitted the original sales receipt instead of a professional jewelry appraisal.

A sales receipt only proves what you paid; it does not describe the quality of the item in technical detail. Insurers require a Retail Replacement Value (RRV) report, which specifies what it would cost to replace the item today at a typical retail outlet. A receipt lacks the "insider" data, such as the exact quality, treatment, or specific details, needed to prove the value of a stone.

The Fix: Request a formal Retail Replacement Value (RRV) report from a qualified graduate gemologist (GG). This document provides the technical 'blueprint' of the piece, establishing a legal valuation that protects you far better than a simple proof of purchase.

2. The "Set It and Forget It" Trap (Outdated Valuations)

I recently saw a client who hadn't updated her ruby ring appraisal since 2012. In that decade, gold prices fluctuated wildly, and the market for high-quality natural rubies shifted significantly. If she had lost her ring, her insurance payout would have been thousands of dollars short of the current market reality.

Market volatility is real. I recommend updating your appraisals every 2 to 5 years. This ensures your coverage limits match the current cost of materials and labor.

The Fix: Schedule an "appraisal" appointment. At Gemology Resources, we keep digital records of your previous appraisals, making updates efficient and precise.

3. Generic Descriptions that Lead to Inferior Replacements

If your appraisal simply says "1-carat diamond ring," your insurance company is likely legally allowed to replace it with the cheapest 1-carat diamond they can find. This is where most people lose money.

A professional valuation must include:

Exact Carat Weight: Measured to the second decimal place.

Color and Clarity Grades: Using GIA or similar industry-standard nomenclature.

Metal Fineness: Whether it is 14K, 18K, or Platinum (PT950).

The Fix: Ensure your appraiser provides a detailed description. This acts as a "blueprint" for your jewelry. If the stone is ever lost, the insurance company must replace it with a comparable item within a reasonable time.

4. Over-valuing for "Peace of Mind"

It’s a common myth that a higher valuation is better. Some unethical appraisers will inflate values to make the customer feel like they got a "deal." However, over-valuing your jewelry only leads to higher monthly premiums.

Most insurance policies are "Replacement Cost" policies, not "Agreed Value." This means if you insure a ring for $10,000 but the insurance company can buy a replacement for $7,000, they will only pay the $7,000. You will have paid years of premiums on a $3,000 "ghost" value that never existed.

The Fix: Ask for an objective, market-based valuation. At our gemological laboratory, we use real-time market data to ensure your valuation is fair and accurate.

5. Failing to Identify Synthetic (Lab-Grown) vs. Natural

In 2026, the distinction between natural and synthetic (lab-grown) diamonds is more critical than ever. Synthetic (lab-grown) diamonds, often created via Chemical Vapor Deposition (CVD) or High Pressure High Temperature (HPHT), can look identical to the naked eye but have drastically different market values.

I have seen many cases where a "natural" diamond was actually a high-quality synthetic (lab-grown) stone. Without advanced technology like spectrometers, even an experienced jeweler can be deceived. If you are paying "natural" prices for insurance on a synthetic (lab-grown) stone, you are being overcharged.

The Fix: Verify everything. Ensure your appraiser has the equipment to distinguish between synthetic (lab-grown) and natural diamonds.

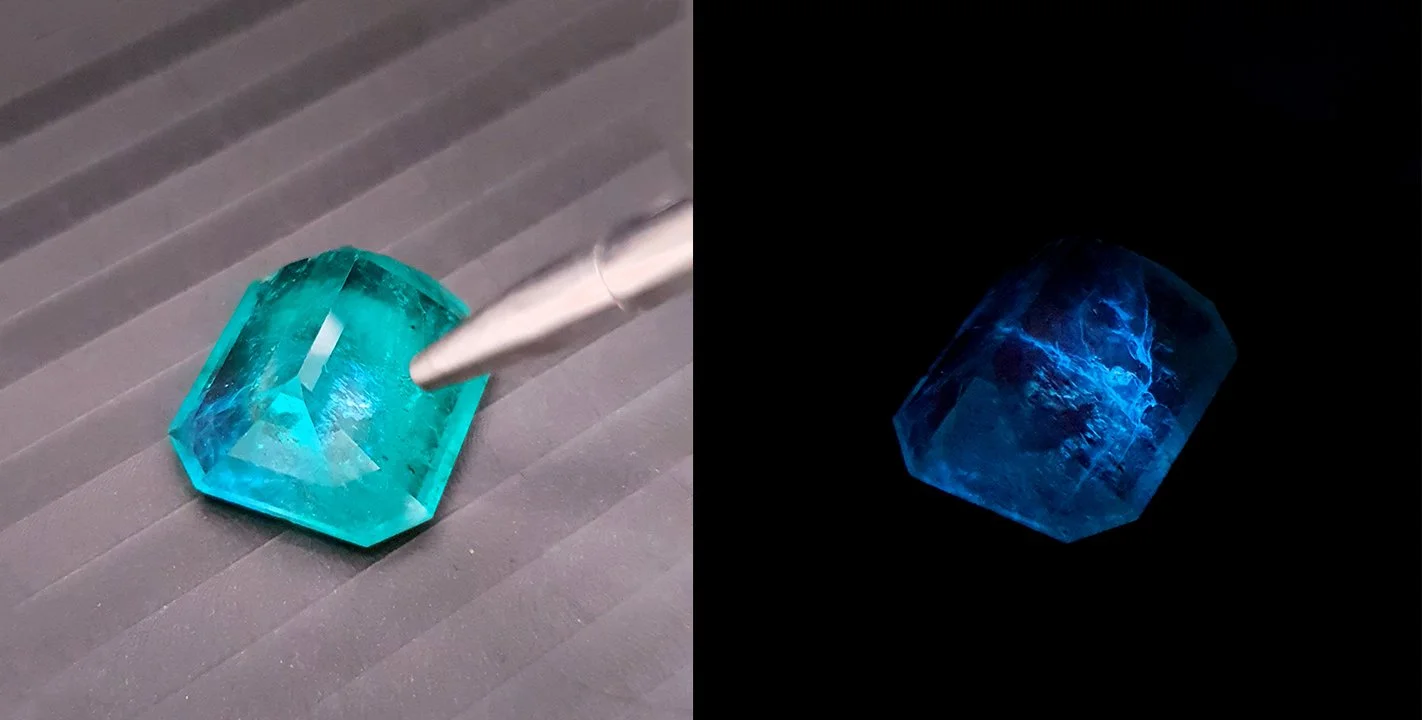

6. Missing Gemstone Treatments (Heat/Fillers)

The value of a ruby, sapphire, or emerald can increase significantly if it is found to be untreated. While most colored stones undergo treatment—which is stable and industry-accepted—it is exceptionally rare when a beautiful stone is untreated, adding immensely to its value and rarity. Most retail appraisals fail to disclose these details because they lack the training and laboratory equipment to detect them.

During an inspection, we look for features that can tell a story of the stone from the earth to the bench. If this lack of treatment isn't noted in your valuation, your insurance coverage is inaccurate.

The Fix: Ask your graduate gemologist: "Has this stone undergone any treatment?" At Gemology Resources, we provide advanced gemstone testing specifically to identify these value-altering treatments.

7. Hiring a Retailer instead of an Independent Graduate Gemologist Appraiser

Many people get their appraisals from the same place they bought the jewelry. While convenient, this is a conflict of interest. A retailer has an incentive to justify the price they charged you.

Be cautious of "appraisals" that are printed on the store's letterhead without a signature from a graduate gemologist affiliated with an organization like the American Society of Appraisers (ASA). An independent appraiser has no stake in the sale and provides a neutral, objective valuation.

The Fix: Look for credentials. I am proud to be a Graduate Gemologist and a member of the American Society of Appraisers (ASA). These aren't just titles; they are a commitment to ethics and continuing knowledge.

A Professional’s Perspective

Your jewelry is more than just metal and stone; it’s an investment. My job is to help make sure that if something happens, you aren't left arguing with an insurance company over a poorly written document. Verify your documents, update your values, and make sure your jewelry is described clearly and accurately.

If you are unsure about your current valuation, I invite you to make an appointment and visit us at our Houston office. We combine experience, careful documentation, and the right tools to give you the clarity and protection you deserve.